and Advance Income Tax (AIT): Explaining Circular SEC/2026/E/04")

: Key Takeaways from IRD Notice PN/SSCL/2026-04/1")

")

")

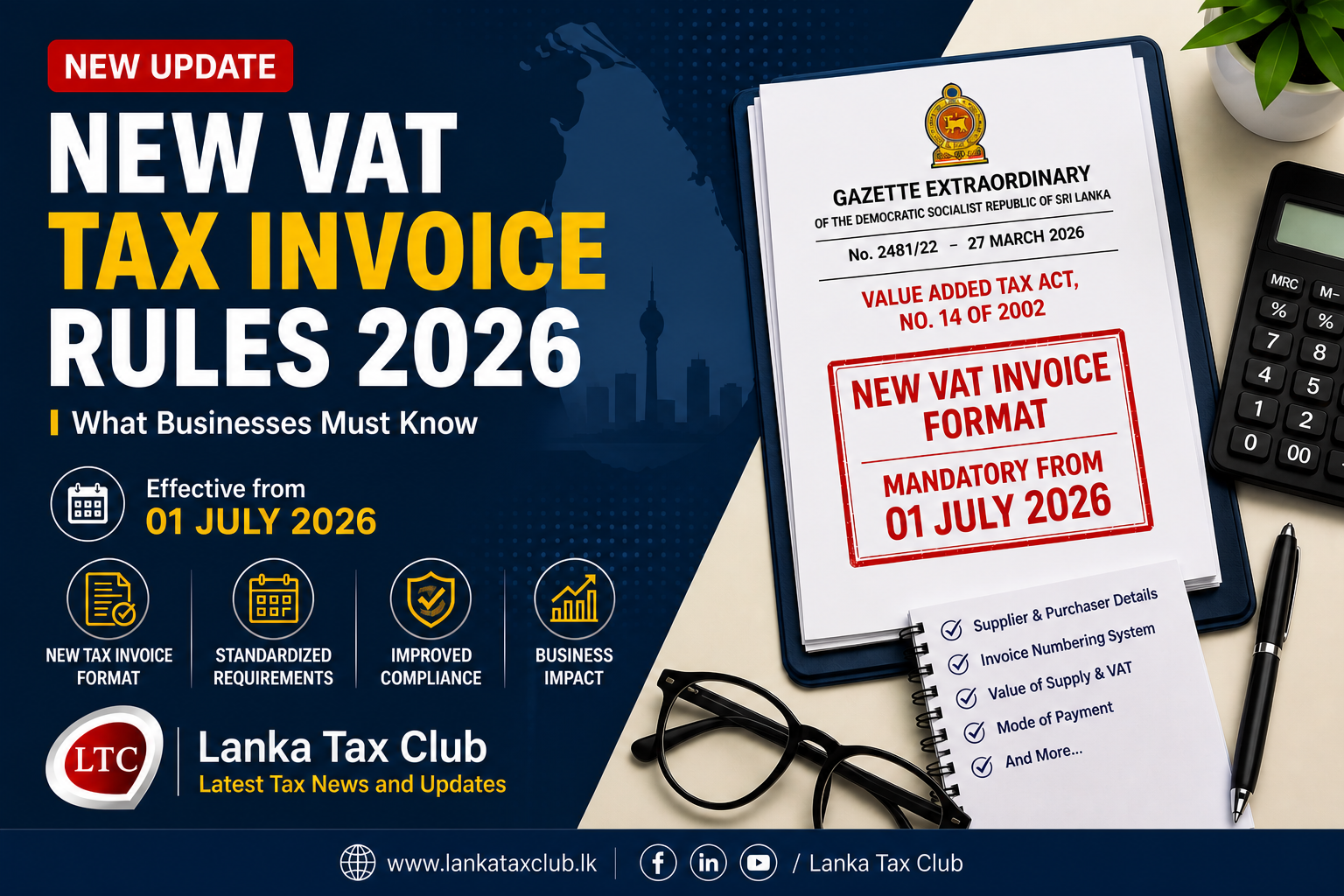

The Hook: A New Era for VAT

For decades, VAT compliance in Sri Lanka has been defined by the tedious manual entry of invoice data—a process ripe for human error and administrative friction. Finance teams have historically operated in a “lag” state, reconciling records weeks after transactions occurred. This traditional model is now being dismantled. Under the National Budget 2026 directive, the Government of Sri Lanka has mandated the implementation of a National e-Invoicing System. This shift represents more than just a technical upgrade; it is a fundamental move toward real-time digital integration. By connecting Enterprise Resource Planning (ERP) systems directly to the state’s tax infrastructure, the Inland Revenue Department (IRD) is eliminating the reconciliation gap and ushering in a transparent, automated era of tax administration.

Watch Video

1. The “Death” of the Manual Spreadsheet (Mostly)

The heart of this transformation is the Web API (Application Programming Interface). This technology serves as a secure, direct bridge between a company’s ERP system and the IRD’s Revenue Administration Management Information System (RAMIS).

The strategic advantage of “real-time” transmission cannot be overstated. By transmitting data for Output tax (Schedule 01), Zero-rated supplies (Schedule 07), and Credit/Debit notes (Schedule 04) as transactions occur, businesses can proactively manage their cash flow and VAT liabilities rather than reacting to month-end surprises. This immediate visibility significantly reduces audit risk by ensuring the IRD’s records match the business’s internal books at all times.

“The system aims to: Improve accuracy and consistency in VAT reporting, enhance transparency, reduce manual errors and intervention, and streamline tax administration processes through automated system.”

However, while the goal is the “death” of the spreadsheet, a hybrid reality remains for now. If the Web API fails or if you are dealing with a supplier not yet integrated into the system, manual Excel (CSV) uploads or the RAMIS e-Service interface remain the necessary contingency.

2. The “Review and Approve” Shift for Purchasers

For CFOs, the most profound operational shift occurs in the procurement cycle. In the legacy system, purchasers were responsible for the manual entry of all input tax data. Under the new regime, the purchaser’s role evolves from “data entry” to “data validation.”

When a registered supplier transmits an invoice via the Web API, that data automatically pre-populates the purchaser’s Schedule 02 (purchases) and Schedule 04 (credit/debit notes) within RAMIS. The purchaser must then review these records in the RAMIS e-Service interface to ensure they match internal procurement records before claiming input tax. To facilitate high-volume operations, the system supports the bulk approval of up to 5,000 records simultaneously. Once validated, the status is updated to “Matched,” providing a verified audit trail.

3. The “No-Delete” Policy

A critical technical implication of this system is “digital immutability.” Once a record is successfully transmitted to RAMIS via the Web API, it is permanent. The system does not allow for the direct editing or deletion of submitted data. This enforces a high degree of discipline in accounting practices, as errors can no longer be “fixed” by simply re-uploading a corrected spreadsheet.

The new protocol for corrections is strictly defined:

- Before: Errors were frequently corrected by manually adjusting entries in a CSV file or deleting and re-uploading records prior to the final filing.

- After: Any adjustment for overstated or understated tax MUST be handled exclusively through the issuance of a formal tax credit or debit note, which is then transmitted as a new, immutable record.

4. Why Exporters and the Tea Sector are the Pioneers

The IRD’s phased rollout is a strategic masterstroke, focusing first on high-volume, sophisticated, export-oriented sectors. Phase 1 targets garment export entities, tea export entities, and tea manufacturing entities. This approach allows the IRD to capture the largest tax-yield transactions through a relatively small number of highly integrated points.

A major milestone was reached on May 1, 2026, when Tea Brokers began transmitting invoice and credit/debit note records on behalf of tea suppliers and producers for all transactions conducted through the Colombo Tea Auction. By starting with these vital foreign exchange earners, the IRD is testing the system’s robustness in high-pressure environments before the Phase 2 expansion to all VAT-registered persons.

5. A Fully Integrated Future (Customs and Beyond)

The National e-Invoicing System is the foundational layer of what will become a 360-degree digital tax ecosystem. The IRD has already outlined enhancements to integrate data directly from Sri Lanka Customs.

This integration will eventually close the loop on the entire supply chain by pre-populating:

- VAT Schedule 03: Import data

- VAT Schedule 06: Export data

By utilizing Customs data to automatically fill these schedules, the IRD is removing one of the final manual hurdles in international trade compliance. This seamless flow between government agencies ensures that every facet of a business’s tax profile is visible and verified in real time.

Conclusion: Preparing for 2026

The manual era of VAT reporting is rapidly coming to a close, with the IRD aiming for full integration across all VAT-registered persons by the end of 2026. For the forward-thinking business, the priority must be ERP readiness. Ensuring your internal systems are technically capable of secure API integration is no longer a luxury—it is a requirement for compliance and operational efficiency.

Download Gazette – Click Here

As we move toward the IRD’s vision of “Taxes – For a Better Future,” the question for leadership is no longer if you will digitize, but how quickly your infrastructure can adapt. Is your business technically prepared for the 2026 deadline?