: Key Takeaways from IRD Notice PN/SSCL/2026-04/1")

")

")

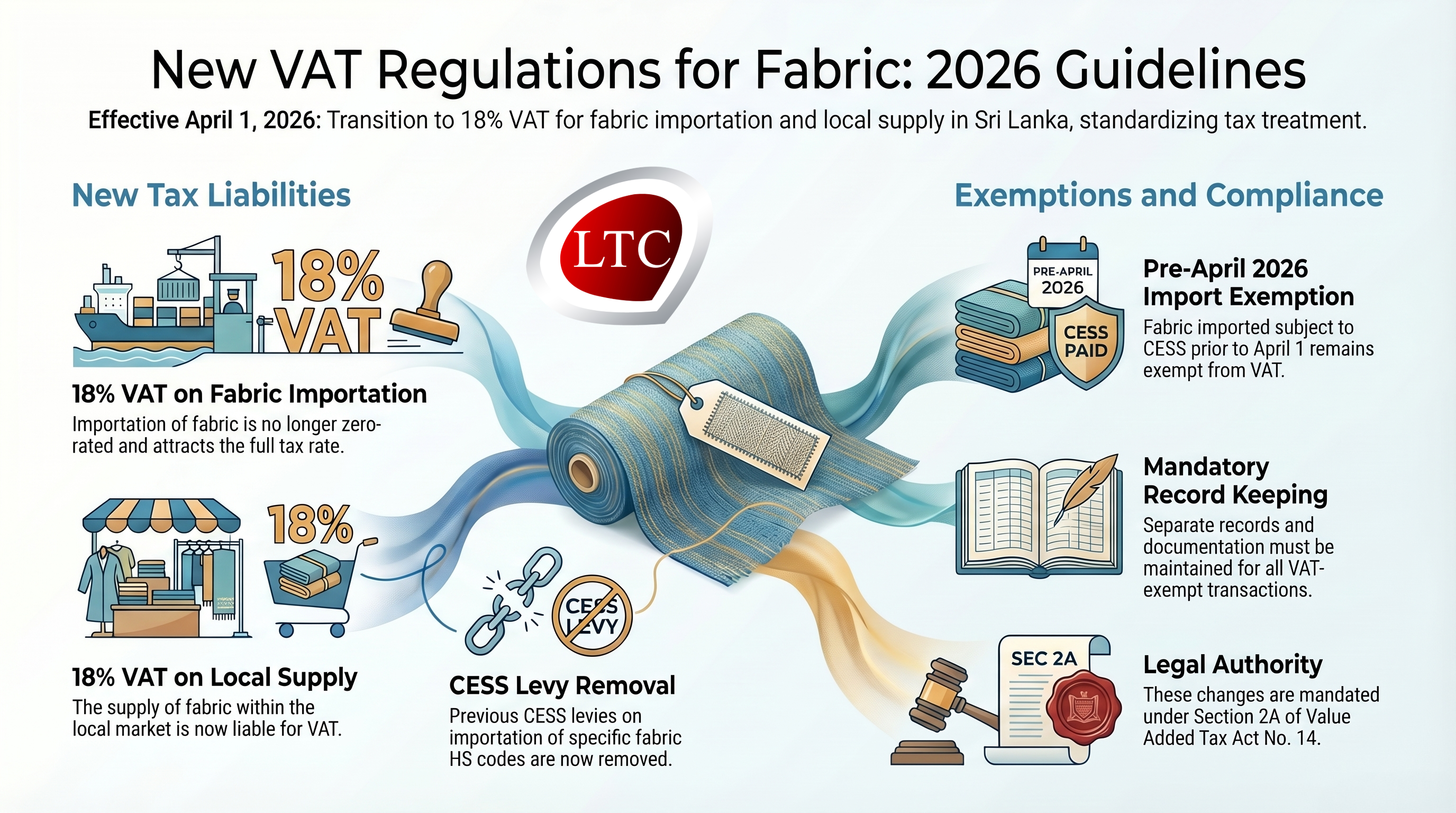

On April 8, 2026, the Inland Revenue Department (IRD) issued a critical notice (PN/VAT/2026-04/1) to all VAT-registered persons detailing a major shift in tax policy for the textile and garment industry. The directive outlines a synchronized change to both the Value Added Tax (VAT) and the CESS levy concerning the importation and domestic supply of fabric.

If your business involves importing, wholesaling, or retailing fabric, it is crucial to understand these new compliance requirements, which took effect on April 1, 2026.

Watch Video

Key Policy Changes Explained

The recent shift is the result of two interconnected gazette notifications that fundamentally alter the tax treatment of fabrics:

- The End of Zero-Rated VAT on Imports: Through Extraordinary Gazette Notification No. 2478/07 (dated March 3, 2026), the Minister of Finance formally rescinded the 2018 gazette that allowed fabric to be imported subject to VAT at a zero rate.

- Removal of the CESS Levy: Simultaneously, via Gazette Notification No. 2479/38 (dated March 10, 2026), the Minister of Industry and Entrepreneurship Development prescribed new goods applicable for the CESS levy. Consequently, the specific CESS levy previously imposed on the importation of fabric under designated HS codes has been completely removed.

- The Domino Effect on VAT Exemptions: Under the First Schedule to the VAT Act, the domestic supply of fabric was previously exempted from VAT if it had already been subject to a specific CESS levy in lieu of other taxes at the point of entry. With the CESS levy now removed on fabric imports, this corresponding VAT exemption no longer applies to newly imported stock.

The Bottom Line: What Changes on April 1, 2026?

Accordingly, the IRD has summarized the new tax reality for the textile sector effective April 1, 2026:

- Imports Attract Standard VAT: The importation of fabric is now strictly liable to VAT at the standard rate of 18%.

- Local Market Supply Attracts Standard VAT: The subsequent supply of this newly imported fabric within the local market is also liable to VAT at the rate of 18%.

- Exemption for Pre-April Stock: Recognizing the transitional challenges, the IRD has included a vital grandfathering clause. If your business is supplying fabric that was imported prior to April 1, 2026, and that shipment was subject to the CESS levy at the time of importation, the supply of that specific older stock remains exempt from VAT.

Compliance Warning: Record-Keeping is Critical

For businesses holding pre-April 2026 inventory, claiming the VAT exemption on local supply is not automatic. The IRD explicitly states that registered persons must maintain proper and separate records and documentation for these specific exempt transactions. Failing to meticulously separate your pre-April stock (exempt) from your post-April stock (taxable at 18%) could lead to audit complications and potential liabilities.