: Key Takeaways from IRD Notice PN/SSCL/2026-04/1")

")

")

The Inland Revenue Department (IRD) has published a crucial Notice to Taxpayers (PN/SSCL/2026-04/1, dated April 16, 2026) outlining significant modifications to the Social Security Contribution Levy. These changes are mandated by the recently enacted Social Security Contribution Levy (Amendment) Act, No. 10 of 2026, which was certified by the Speaker on April 9, 2026.

For the members of the Lanka Tax Club and the wider business community, here is a detailed breakdown of the two primary amendments you need to prepare for:

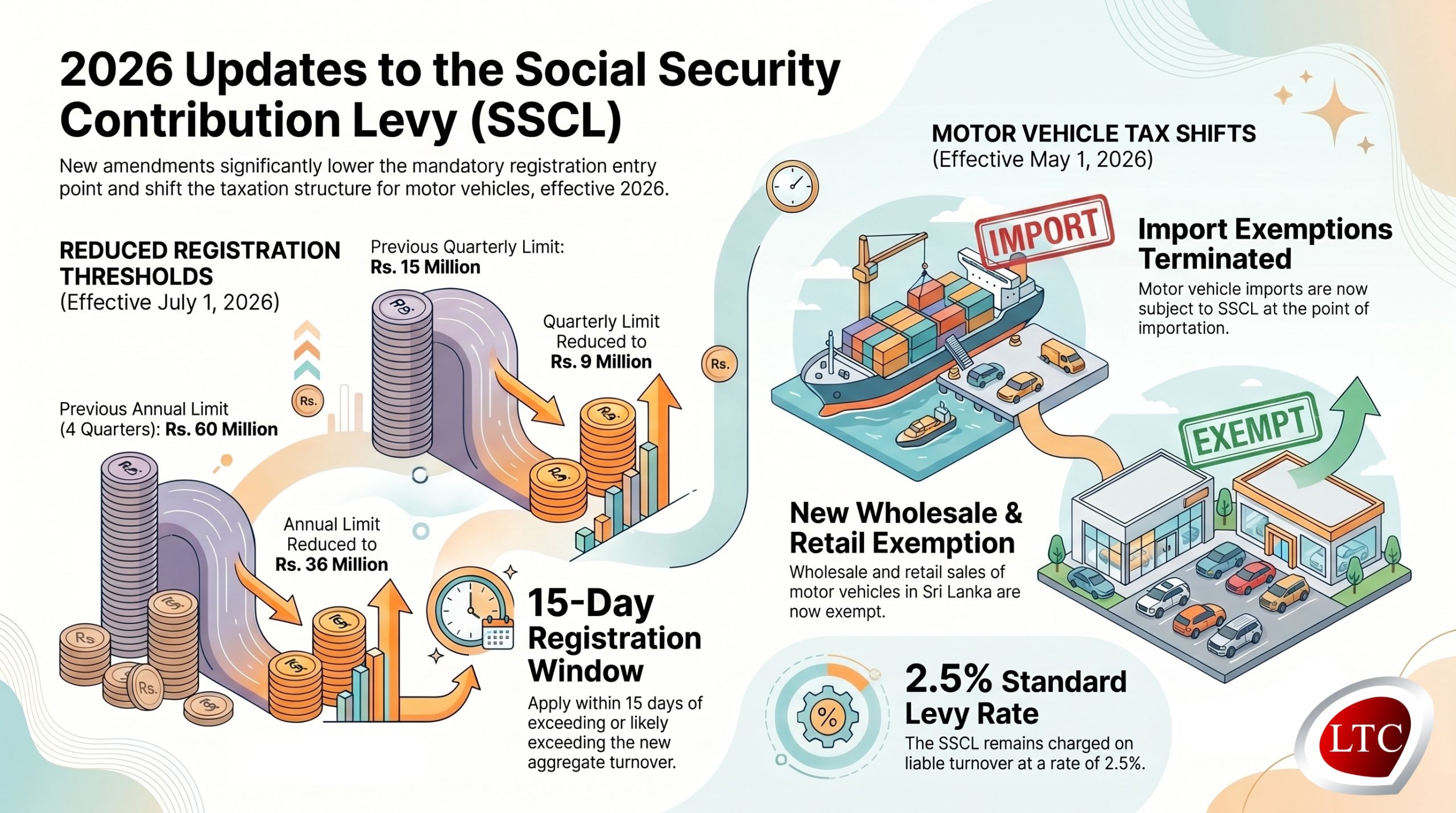

1. Drastic Reduction of the Registration Threshold (Effective July 1, 2026)

In a move that will widen the tax net and bring many small and medium enterprises (SMEs) into SSCL compliance, the aggregate turnover threshold for registration has been significantly lowered.

- The threshold is reduced from Rs. 15 million to Rs. 9 million per quarter.

- The annual threshold limit is reduced from Rs. 60 million to Rs. 36 million for a period of four consecutive quarters.

This rule applies to every taxable person carrying on a taxable activity, with the exception of persons who solely import articles.

Compliance Action Required: If your business’s aggregate turnover exceeds, or is likely to exceed, the new Rs. 9 million threshold during the quarter of July 1 to September 30, 2026 (or any quarter thereafter), you are legally required to apply for SSCL registration within 15 days from the date the turnover crosses or is expected to cross that mark. Once registered, SSCL payments must be made on the liable turnover from that quarter onwards.

2. Restructuring of SSCL on Motor Vehicles (Effective May 1, 2026)

The Amendment Act shifts the point of taxation for motor vehicles from the domestic market to the point of entry into the country.

- Imports Now Liable: The previous exemption that applied to the import of motor vehicles (under Item 25 of PART IA of the First Schedule) has been formally terminated. Starting May 1, 2026, the import of motor vehicles will be subject to SSCL at the point of importation.

- Local Sales Now Exempt: To balance this, the IRD has introduced a new exemption (under Item 7 of PART IB of the First Schedule) which completely exempts the wholesale and retail sale of any motor vehicles in Sri Lanka from the SSCL.

What This Means for Businesses

Automobile importers will need to account for the SSCL at customs starting this May, while local dealerships will no longer have to charge SSCL on their domestic vehicle sales. Meanwhile, businesses across all other sectors must urgently review their quarterly revenue projections to ensure they do not miss the new Rs. 9 million registration threshold starting in July.

[mc4wp_form id=31222]

Download Paper Notice: PN/SSCL/2026-04/1

Stay tuned to the Lanka Tax Club for further interpretations and practical guides on navigating these new compliance requirements.